The high stake gamble

What are the calculations and logic behind the recent moves on the Russian-European gas chess board?

I have just published an article at Carnegie on the latest developments on the gas front between Europe and Russia. Here is an extended version, the director’s cut if you wish.

The great conundrum of the 10 days in July between July 11 and July 21, 2022, was whether Gazprom would turn the Nord Stream 1 pipeline on again after the routine maintenance. The flow interruption per se was not unusual, it always happened for roughly the same period on roughly the same dates since 2013, when the pipeline was put in operation. However, in the past, Gazprom compensated for the flow shortfall through different pipelines and had no apparent reason to find an excuse not to restart. In 2022 from the beginning of May Gazprom was gradually reducing gas supplies to Europe to a third of the usual supply levels. NS1 was curtailed to 40% of the nameplate capacity, ostensibly due to technical issues and problems with getting one of the pump drivers back into its place of service from maintenance in Canada. Polish route, which in the past was used to partially compensate for the NS1 throughput, was sanctioned by the Russian government on the 10th of May 11th, Ukraine declared a war-related Force Majeure on Soyuz pipeline, of the two, delivering Russian gas to Europe via Ukraine, and Gazprom claimed that it could not divert the flow to the Urengoy-Pomary-Uzhgorod. So, by the end of June, five possible routes to Europe for the Russian gas turned into three (Nordstream 1, Urengoy pipeline going via Sudzha and the Turkstream).

There were speculations that in continuation of the trend Gazprom would announce with great sorrow that the annual maintenance has discovered some grave problems with the pipeline that would preclude a re-start and require some difficult, sophisticated, and time-consuming repairs. Nevertheless, gas flow resumed at the planned date and time and at the same (sharply reduced) volumes, as before the maintenance. At the same time, the German government pled the Canadians to bend their sanctions rule and issue a derogation, all in the name of European energy security, and allow the ill-fated pump-driving turbine to get back from the Montreal maintenance facility to Russia and be placed back in service, which should raise the NS1 throughput. Canada relented, the turbine was flown to Hamburg and was prepared for a trip to St. Petersburg.

Europe exhaled with some relief, but not for long. 5 days later, on the 25th of July Gazprom announced that on one hand, it still could not take back the turbine because in Gazprom’s words Siemens could not produce all the required paperwork that would assure Gazprom that accepting the turbine and putting it in operation would not create a violation of sanctions and would not put Gazprom at risk with the Canadian, US, UK and EU regulators and authorities. At the same time, Gazprom announced that it had to take another turbine out of service under orders of the Russian State Technical Inspectorate, as that turbine is also due for service, and is not allowed to accumulate any more working hours before that. As a result, instead of going to the 100 million m3 per day, as hoped, the gas flow dropped to 33 mln. m3 per day or to 20% of the capacity.

Gazprom is still claiming a combination of technical mishaps, regulatory requirements, political circumstances, and other reasons beyond its control with some vanishing degree of plausible deniability. A more likely explanation is that there is an orchestrated effort to reduce gas supply to Europe, as a part of the larger standoff between Russia and Europe and Gazprom has to comply with the orders from Kremlin and come up with ideas of how to play it tactically. By now, there is little doubt that there is an ongoing gas war. But what might be the strategy and considerations of the Russian player, dictating these particular actions?

In the summer, when gas consumption is half of the winter peaks, Europe can do without Russian gas, replacing it with LNG. It requires overbidding everybody else for LNG cargoes, makes gas rather expensive for Europe, and already causes problems for countries like Pakistan, which cannot afford to buy it anymore, but that’s another issue. It also hurts the European economy, which is already balancing on the edge of recession and trying to tame inflation, unseen in decades, but again, this is yet just a problem of less wealth and slower economic growth.

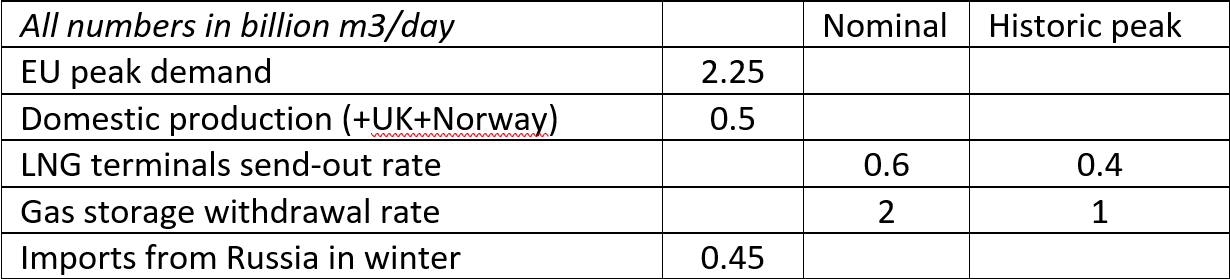

In winter, however, even with the storage full and all the European LNG terminals working at full capacity, Europe would still need at least some Russian gas and – during a cold spell – a substantial amount of Russian gas to keep lights on, homes warm and industry working. European gas distribution network has been built to feed gas from the east to the demand centers. This general flow direction was augmented by LNG terminals, mostly still in the west of the continent, additional eastbound pipeline capacity, and gas storage in Central Europe, but still there are pipeline network bottlenecks and gas send-out rates of the LNG terminals and storage reservoirs are limited, which likely would not be enough to cover peak demand.

This is illustrated by the table below:

(data from

- https://alsi.gie.eu/

- https://agsi.gie.eu/

- https://www.iea.org/data-and-statistics/charts/estimated-daily-gas-consumption-in-europe-during-the-heating-season-2019-2020-and-2020-2021

- https://www.bruegel.org/dataset/european-natural-gas-imports )

Much of the LNG capacity is concentrated in the areas, poorly connected to the pipeline network. For example, 0.2 bcm/d of LNG send-out capacity is in Spain, while there is only 0.02 bcm/d of pipeline capacity from Spain to France.

And if storage is less than full, there would be not enough gas to not only cope with the peak demand, but to go through the winter as well. This situation will put the basic well-being of the European population at stake and will require tough and unpopular decisions from the governments – such as energy rationing and industry lockdowns.

Scenarios of Russian export shutdown have been evaluated by the European Commission Energy directorate and ENTSOG since 2014 with the last one concluded in the Fall of 2021

Interestingly enough, while the initial report from 2014 focused on the all-out shutdown of the Russian supplies, the later versions, while more detailed, only considered a number of scenarios, contemplating a disruption on a single route.

The 2014 study sounded like “Not great, not terrible” – yes there will be some temporary problems here and there, some administrative measures and rationing might be required, and burden sharing will be needed, but in general, Europe would manage to get through the winter without Russian gas. These studies do not look at the economic effect and the costs of countering measures but only at physical security of supply and technical means of coping. The difference between 2014 and 2022 though is that since then European domestic gas production went down by 50 billion m3 per annum, while consumption went up by the same 50 billion m3, according to BP Statistical Review of Energy. Another important element in the 2014 study was that it assumed a disruption starting in November, i.e., going into crisis with full storage.

Russian politicians are firmly convinced that Europe would need Russian gas to go through the coming winter. In Russian strategic calculus, this challenge will either make the European governments call for a truce in the trade war, cut support and weapon deliveries for Ukraine, and restore normal trade relations with Russia, or will have to face a severe economic and political crisis - splintering of European unity and solidarity, conflicts between European countries for scarce resource, just like there were bans on movements of crucial goods between Soviet republics in the 1990-1991. This political crisis might bring populist and opportunistic forces, such as AfD in Germany and NFP in France, to power and they would be willing to cut separate deals with Russia, giving it in the end what it wants by hook or by crook.

This plan viability calls for low levels of gas in storage, comes a heating season, thus it is important for Russia to keep the filling rate now as low as possible, and this might be the main rationale for the gas supply curtailment since the beginning of June. But why would Russia then restore the Nordstream flow, even at the reduced levels, instead of cutting all gas supplies completely? What’s the point in mockery and cat and mouse games?

There are a number of reasons why Russia might want to maintain some gas sales to Europe.

First, there are practical considerations. It will be easier to restore the levels of trade to normal levels than to re-establish a trading relationship from scratch. Pretending that Gazprom does everything that is in its power, might help in future dispute resolutions and arbitrages (and there likely will be a number of suits for damages from undersupplied Gazprom counterparties). This problem could also be circumvented by the government issuing a ban on gas sales to unfriendly countries, and Gazprom calling a Force Majeure based on such an edict.

There is an economic reason – with gas prices in Gazprom contracts now linked to the hub and index prices, Gazprom enjoys high revenues from low sale volumes, so it is having and eating its cake. If the supplied volumes are low enough to not avert the winter crisis, why not then add the insult of making the Europeans pay Gazprom to the injury in making?

There is some propaganda value in keeping some gas supply. Russia is saying at the moment, that European gas blues are self-inflicted, and addresses this message to the European population starting to feel the rising gas prices and fear of gas shortages.

Keeping gas supplies at some levels also allows for divide et impera and the creation of discontent amongst Europeans – Russian-friendly Hungary, for example, will most likely keep its gas supply (and at very favorable prices) till the last possible moment, and its example will be trumpeted to the struggling citizens of other European countries, if not by the Russian propaganda, then by their own populists.

There is also a reason for the calculated application of pain and measured spending of the economic warfare arsenal on the Russian side. A complete gas flow shutdown is the strongest weapon that Russia could use, and it is probably more valuable as a threat. There will be few other measures that Russia could use after that, no sizeable further escalation steps, and would place Russia at a disadvantage in a protracted conflict.

At last, this mockery just fits the general behavior pattern and rhetoric of the Russian politicians in the last years – the behavior of a nonchalant youth, challenging a teacher or a constable, pretending to be formally correct, but actually nasty, trying to ridicule and bully everybody around him in a hope of getting some respect – out of fear and pain from the outsiders, out of awe at his bravery and cheekiness, from the junior members of the street gang.

Russian-European gas trade is a 50-year relationship, that survived the Cold War and break-up of the Soviet Union and brought a steady flow of income to Russia. At the moment Russia has no other way to monetize this gas, at least until a new pipeline to China would be built, which would take several years. Is it really worth using it just as an expendable chip in the game and destroying its future value? There is a number of reasons.

From the Russian standpoint, Europe was playing unfair and opportunistic since the beginning of the 2010-s, after the Third Energy Package went into force and European energy companies started to demand changes to the long term contracts and taking Gazprom to arbitrage over these demands. The Russians have seen the arbitrages bringing judgements in favor of the European companies and Naftogaz of Ukraine as biased and held grudges against it. Growing European shift away from combustible fuels towards renewables, prospects of the American LNG coming to Europe en masse after 2025 (in the Russian eyes – for political reasons and as a result of unfair competition) – these developments also reduced the going forward residual value of the gas trade with Europe for Russia, despite all the skepticism over the Energiewende and competitiveness of the American LNG.

On the other hand, there is probably a belief that when Russia wins in the whole conflict or at least achieves an honorable peace settlement, the gas trade will be a part of the overarching comprehensive agreement with the West, which would include a long-term gas sale and purchase agreements, forgiveness of all the possible damages and claims stemming from the non-fulfillment of the contract volumes and settlement of any other issues arising along the way. And if Russia loses… Well, for Putin and his team the destruction of the gas trade and possible claims would be just one of the smaller problems to think about. So, there is every reason for them to raise the stakes and put that chip on the table.

Thanks for the analysis, and precise description of Russian establishment’s behaviour. Gas consumption in Europe is reducing which makes the goal of 80% of storages capacity filled by Nov. 1 more achievable. Do you believe in that scenario? Because if that will be the case, then Russia will have to stop gas supplies completely to achieve the desirable effect.